Further Thoughts on the Business of Football

Last week I published an essay in the Bloomberg Odd Lots newsletter about financialization and football, co-authored by my podcast co-host Mike Goodman. We used the recent financial shenanigans at Chelsea and Barcelona to dig into questions of exactly what the business of football is, for the owners of football teams.

I’m pretty happy with how the essay came out, and you can read it here.

In this newsletter, I wanted to expand on a few points from our conclusion. The core of the piece is an overview of the many ways that Barcelona and Chelsea have attempted to hide their year-over-year losses via financial tricks and accounting maneuvers, and how they have ultimately been successful in evading consequences from their leagues’ financial regulators. The essay ended up growing into a larger disquisition on the state of football as a business and I think summarized the basic ways in which Mike and I have been thinking about football business and discussing it on the Double Pivot podcast.

Chelsea’s and Barcelona’s financial schemes raise an obvious question. Why would anyone want to get involved in a business where you lose so much money every year that you have to deploy financial engineering to hide some of your losses?

Obviously, some people would do it because they want to see a particular football team win matches and they’re happy to see the wealth they’ve accumulated over their lives diminish to make it possible. And some people would do it because they controlled the sovereign wealth fund of an oil state and that state wanted to establish a soft power foothold in Western Europe. And some people would do it because the money they looted from the collapse of the Soviet state made them incredibly rich but the new Russian dictator they helped bring to power could threaten their wealth and safety if they couldn’t move it out of Russia, and buying a football team in London could help establish themselves and their portfolio securely in a society outside that dictator’s reach. There are real exceptions, which I will come back to.

But most of the people and organizations that buy and own football clubs articulate some business reason for purchasing a club. Certainly Clearlake Capital, the new majority owners of Chelsea, are not acting out of generosity toward the people of West London. So what is the business of football at the level of club ownership?

These two paragraphs from our article form the core of my understanding of these dynamics.

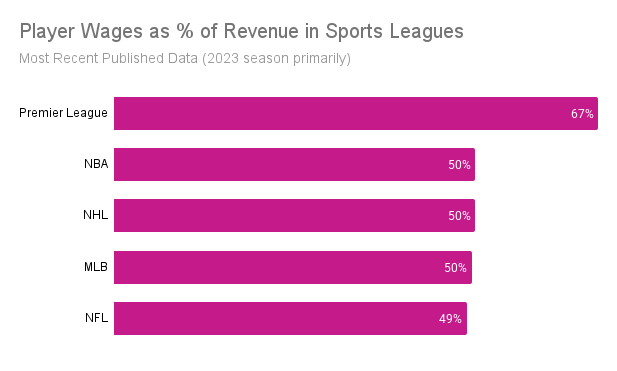

The first key point is that the business case for owning a soccer team has never depended on profit-making. Premier League clubs reported 777 million pounds in losses in the 2023 season despite revenues greater than any other soccer league in the world. In North American sports, most owners can expect regular profits because of the cartel system of fixed leagues. Collective bargaining in these systems means that wage costs can be set as a percentage of revenues league wide. Competition between leagues in Europe, and competition to avoid relegation to lower divisions, has led to significantly higher relative overall labor costs. Wages in the Premier League in 2023 ran at about 67 percent of total club income, while in North American sports this number typically runs between 45 to 55 percent, and with the added certainty that comes from collective bargaining agreements.

Where owners have made money in soccer is through asset price appreciation. When Roman Abramovich was forced to sell Chelsea in 2022, he was paid 2.5 billion for the club. Abramovich purchased Chelsea in 2003 for 140 million, which calculates to roughly 16 percent yearly growth, or 13 percent adjusted for inflation. Other sales tell a similar story. In 2005, the Glazer family completed the purchase of Manchester United in a series of deals finally valued at 790 million pounds, and they sold a 25 percent stake in the club to Jim Ratcliffe in 2023 for 1.3 billion. That calculates to eleven percent yearly growth, or eight percent adjusted for inflation. Interested owners might plausibly look at both of these growth rates as undervaluations of their expected returns. Abramovich took those profits in a forced sale in which he did not even legally control the entity at the time it was sold. The Glazers loaded Manchester United with a half-billion in debt in their leveraged buyout takeover and have overseen some of the famous side’s worst-ever performances, yet the club’s valuation still grew more than six times over in 18 years.

Football clubs consistently lose money. Even the most successful league in the world sees year-over-year losses in the aggregate running toward three-quarters of a billion pounds. And they lose money for extremely straightforward reasons. While North American sports leagues have mostly capped the percentage of revenues that go to player salaries through collective bargaining,1 the competitive structure of European football has prevented any such limitations on labor costs.

But despite this, the value of Premier League clubs at sale keeps going up at eye-watering rates.

Football clubs, for the last couple decades, can be understood as financial assets which consistently lose money year over year but appreciate at a rate that typically swamps these losses. This is the structure of a bubble, more or less. But it has been a couple decades, and the bubble has not popped.

One trend which has clearly powered the continued growth of football club valuations has been the spectacular growth of football revenues. Across the affluent world, people have been spending more and more money on sports for a few decades. This trend may finally be levelling off, as can be seen in the English Premier League’s domestic television revenues.

The 2016 domestic TV deal still stands as the best deal the Premier League has negotiated in yearly revenue terms, even without any adjustments for inflation. Grace Robertson wrote an excellent essay on the history and current state of the Premier League’s television revenue, making the case that we have probably hit a market top. Overseas revenues do continue to grow, with the most recent set of deals estimated at a 30 percent increase, but even that is significantly less rapid growth than was common over the last few decades.

There has been a coherent argument that it makes sense to buy into a growth industry like sports in the belief that eventually these revenues can become consistent profits. But despite the argument, that has not happened in European football. Labor costs remain elevated and these seem to be few paths to the consistent profits of North American sports teams which typically pay about 50 percent of revenues in wages.

One thing that Mike pointed out to me as we were writing the article is that the structure of football club ownership, where you pay some year-over-year losses to lock in longer-term asset valuation gains, also looks more appealing in the low or zero-interest rate environment of the 2010s. Once government debt offers substantial, safe yields, a football club starts to look like a less appealing place to park money for a while.

I think this situation probably leaves club ownership at a crossroads. They can either figure out a way to drive down labor costs as a percentage of revenues or they can see their glorious asset appreciation curve level off while still paying down yearly deficits. This is the core of the European Super League drive, and why it was supported by the ownership groups of Liverpool, Manchester United, Arsenal and Tottenham. A fixed league offers the opportunity to collectively bargain with labor rather than constantly competing across national borders for talent. Removing the threat of relegation excises from the game the death spiral logic of running losses in order to avoid running even larger losses the next season in a lower league. The Super League push decisively failed, however, and little in the game over the last few years has suggested any trend toward serious wage limits.

Now, one of the reasons the Super League failed, along with the fan protests from below, was the refusal of Paris Saint-Germain to go along with the plan. There is no need for a club owned by the sovereign wealth fund of Qatar to get into a fight with UEFA just in order to limit its losses. Those losses are a small price to pay for the soft power gains of club ownership. Manchester City, owned by Sheikh al-Mansour of the United Arab Emirates, was then among the first clubs to back out of the Super League.

This can be read in two ways. First, the existence of nation-state ownership may fatally undermine the class solidarity of club owners. As football clubs and leagues have continually sought out new sources of wealth to cover their losses, they found massive gains in bringing in oligarchic and nation-state actors who would happily eat losses while providing huge payouts to exiting ownership. But now these folks have seats at the table and they do not prioritize driving down labor costs as remotely the same kind of existential goal as their fellow owners.

I remain deeply skeptical of the business logic of club ownership, and in particular of the possibility of the kind of systemic reform that would be needed to lock in lower labor costs. The ownership class lacks the kind of solidarity that has benefited owners in North American sports leagues, and this sort of solidarity is difficult to build. Without any path to controlling labor costs, the continued growth of football club valuations still looks like a bubble. This is an economy where people lose money every year and then make it back by selling off the money-losing assets to new buyers. If I were advising a wealthy consortium I would try my best to steer them away from club ownership.

But the same nation-state ownership that seems to be undermining the case for cost controls also might point to the source of new funds to keep the market whirring. What if three exceptions I outlined at the beginning of the newsletter can serve as a source of asset appreciation? That is, perhaps there are still a few more state-backed ownership groups still to buy into the top divisions of European football. Perhaps some new class of international oligarch will emerge in the coming years looking to move wealth across borders. And perhaps the appeal of owning a football team will continue to convince wealthy individuals who should know better to commit large bids at the next auction. There is probably still more wealth out there to buy into club ownership for non-business reasons. There are surely still new sources of irrational money, wealthy individuals reading to buy into bad arguments for these purchases because they’re talking themselves into buying a new toy.

The reason to bet against the bubble popping is a deceptively simple one. People love sports. Football is the most popular sport in the world. Owning one of the most famous football clubs in the world offers a path to recognition at the highest levels of society for people and states who would pay anything for the privilege. And owning a football club offers a possibility of excitement and joy that more rational investments typically cannot. The market for football club ownership then should be understood a kind of perpetual motion machine, driven by the irrational attachments of sports fans from every level of society.

Collective bargaining, of course, ensures the players a say in league business and guarantees an array of labor rights.